FiDA – The path to open finance?

From open banking to open finance. The Financial Data Access Regulation (FiDA) aims to make this possible. Customers will be able to decide for themselves who has access to their financial data, while financial institutions and insurance companies will have to review their systems, data processes, and interfaces. The challenges are considerable, but FiDA opens up enormous opportunities: new data-based business models, innovative services, and more competition in the European financial sector.

FiDA is no longer a theoretical concept, but has arrived at the heart of the European legislative process. Trilogue negotiations are currently underway and are expected to be concluded in the first half of 2026. These discussions focus primarily on practical issues: How far should data access actually extend, and how high should the technical and organizational requirements be? Nothing has been finalized yet, but one thing is clear: We are heading in the right direction. FiDA is coming.

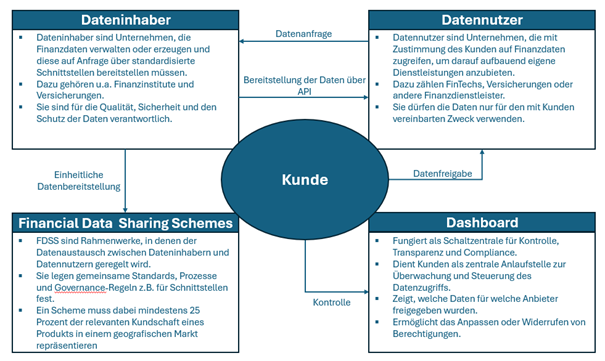

With FiDA, the EU is pursuing the goal of fundamentally reorganizing access to financial data and going beyond open banking to open finance. Customers should be able to decide for themselves which of their financial data they share with which providers. At the same time, a uniform European framework is to be created that breaks down data silos, promotes competition, and enables innovation in the financial sector. Through standardized rules and interfaces, FiDA aims to create a level playing field for established institutions and new providers, thereby promoting new, data-based business models.

FiDA focuses on customer data from financial companies and insurance providers. They decide whether and for what purpose their financial data is shared. Data owners such as banks or insurance companies provide this data and ensure secure and standardized access. Data users use the shared information to offer new services based on it. Data exchange should be based on uniform rules and technical standards to ensure transparency, security, and control.

For banks, insurance companies, and other financial institutions, FiDA already presents demanding challenges, the specific form of which, however, depends largely on the ongoing trilogue negotiations. It is clear that IT systems will have to be adapted and interfaces more standardized in order to enable secure and reliable data exchange. At the same time, issues such as data management, data quality, and timeliness are becoming more important, especially in light of possible real-time requirements.

Data governance and compliance requirements will also become increasingly important with FiDA. Responsibilities, approval processes, and control mechanisms must be transparent and traceable in the future. FiDA affects not only individual applications, but potentially an institution's entire data platform—from architectural issues and access controls to monitoring and operation. Which specific standards and transition periods will ultimately apply will only become clear once negotiations have been concluded.

CURENTIS AG supports banks, insurance companies, and other affected companies in this early phase with strategic and technical preparations for FiDA. We analyze existing IT and data landscapes, identify potential areas for action, and provide support in aligning systems and processes so that they can flexibly meet future regulatory requirements.

Due to the fact that some points of the FiDA are still under political discussion, it remains to be seen what the final regulations will look like and what concrete effects they will have on market participants. However, it is foreseeable that FiDA will bring about lasting changes in the use of financial data. We are keeping a close eye on the current developments in the legislative process and will provide timely information as soon as there are any significant changes to the draft version.

To the author:

To the author:

Artur Kehrein has been a Senior Consultant at CURENTIS AG since 2022. He has many years of experience in risk management and regulatory reporting. He also specializes in sustainable/green finance and regulatory reporting.