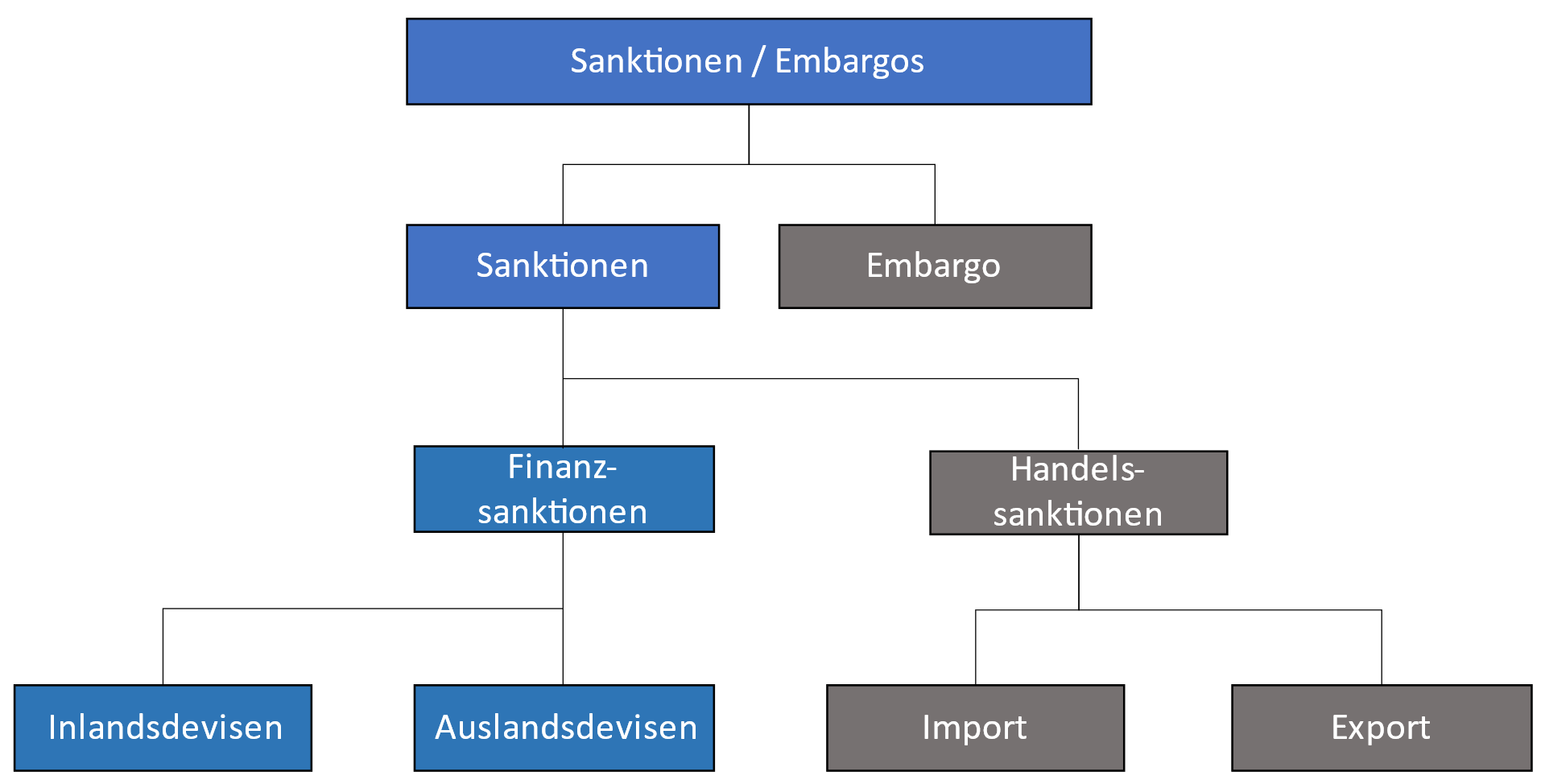

Financial sanctions and tactics to circumvent them

Against the backdrop of the Russian attack on Ukraine and the resulting sanctions imposed by America, the EU and Switzerland, the hoped-for effects and undesired side effects of sanctions are a very topical issue. As part of our series of articles on this topic, we describe financial sanctions and their mitigation in this article.

In this article we describe the blue highlighted issues around financial sanctions affecting domestic and foreign foreign exchange.

Forms of financial sanctions

While trade sanctions often target specific goods, countries or regions, financial sanctions tend to focus on private individuals. The current financial sanctions against a growing list of Russian oligarchs are at the center of efforts to put pressure on the Russian government.

In contrast to trade sanctions, financial sanctions are more difficult for private individuals, banks and companies to avoid. This is mainly due to the global networking of payment systems and the strict supervision of banks. Nevertheless, there are ways and means to circumvent financial sanctions as well. In the remainder of this article, we will highlight some of these tactics with the help of examples.

An exception to targeted financial sanctions against private individuals are financial sanctions applied to entire states and their central banks. For example, the Russian Central Bank has not been allowed to trade on Western financial markets since late February, and Russian banks have been excluded from the SWIFT payment system. (Euronews, 2022)

States can impose financial sanctions by prohibiting sovereign and intergovernmental lending to targeted countries. In addition, trade finance can be disrupted by classifying sanctioned states as non-cooperative or as having a primary money laundering problem. This hurts the sanctioned country's economy through higher interest rates, and there is a risk that financing will dry up as creditors seek to avoid the additional credit risk or the risk of being sanctioned themselves. Financial sanctions between central banks also affect trade, as financial institutions are no longer willing to participate in trade finance. Thus, trade can be affected without explicitly imposing trade sanctions.

Sanctions may also take the form of asset freezes. The assets of the sanctioned target, whether an individual, legal entity, or state, are withheld or "frozen" so that the sanctioned target cannot access or use them. This usually takes the form of frozen bank accounts or other assets. These sanctions deprive the sanctioned individuals of their money.

The example of the ruble exchange rate shows very clearly how effectively financial sanctions between central banks can influence the economy of a sanctioned country. The Russian central bank has already started to increase its foreign reserves since the annexation of Crimea in 2014. In 2014, for example, the Russian central bank had the equivalent of nearly $270 billion invested in foreign currencies. Then, on February 24, 2022, a tweet surfaced purporting to put the lineup of Russian foreign currency at over $630 billion. Due to the Western sanctions implemented as of February 2022, over 60% of Russia's foreign reserves have been frozen. This news resulted in a drop in the ruble's exchange rate of up to 42%, which the Russian State Bank responded to by raising the key interest rate from 9.5% to 20%. In addition, the Russian government has attempted to require gas payments in rubles to support the ruble. Even if the effect of these measures cannot be calculated precisely, the ruble has stabilized in the meantime. Whereas in March the ruble was worth 144 rubles per euro, by the end of April it was worth only about 76 rubles per euro.

Examples of sanction avoidance

In the following, we present two tactics for sanctions avoidance that are very likely also used by Russian actors in the international financial market to circumvent Western sanctions. The first tactic relates to transactions between banks in foreign currency and thus has an impact on the strength of the domestic currency. The second tactic is one that is very often used by sanctioned individuals.

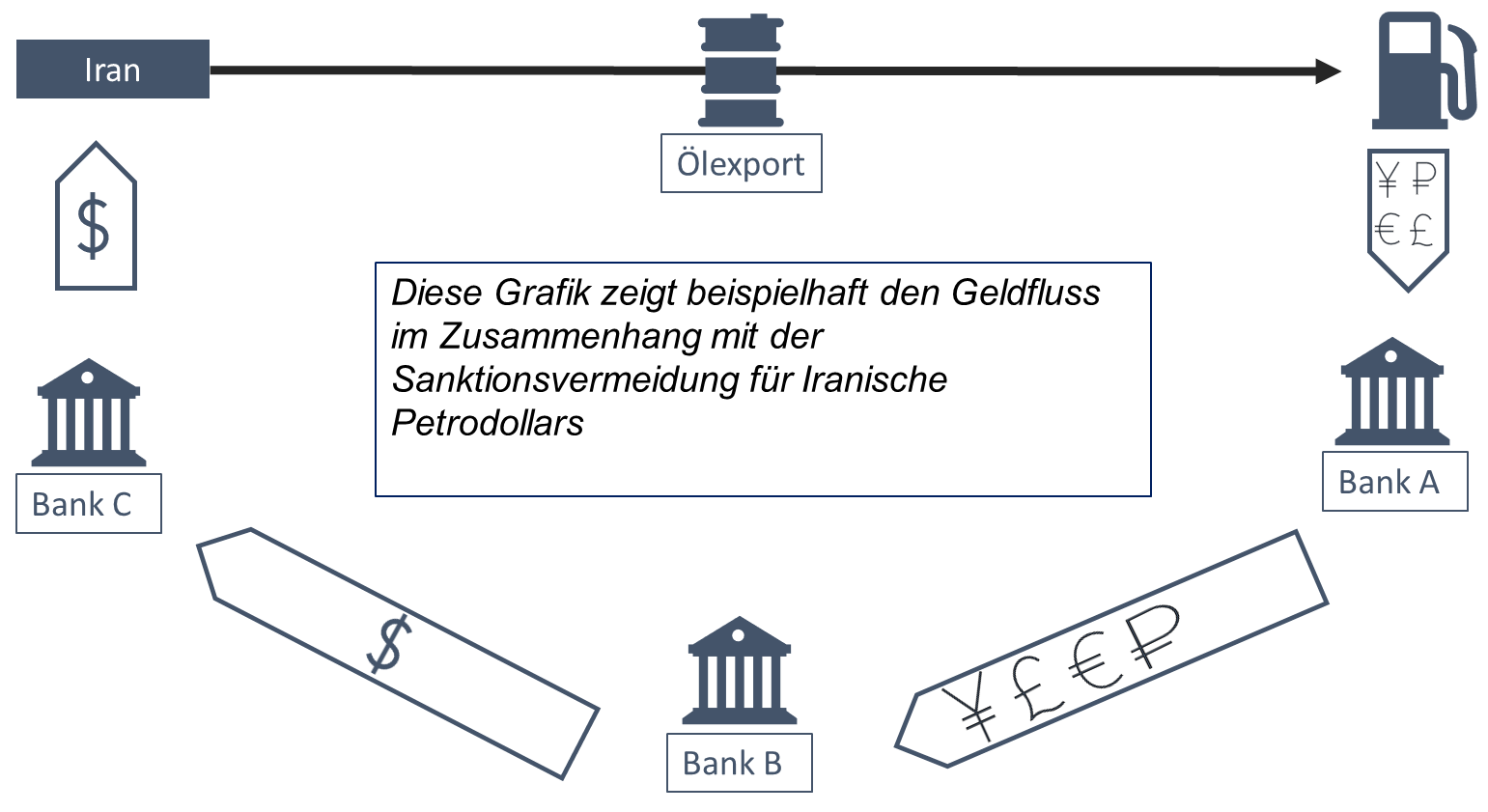

1. u-turn payments for Iranian oil

U-turn payments are payments made across multiple banks, across countries, and are often related to changed or missing payment information.

The transactions are transferred from bank "A" via bank "B" and "C" to the sanctioned country. The bank that avoids sanctions in this case is bank "A" by transferring money to a sanctioned country via banks "B" and "C" in a prohibited manner.

This tactic of sanction avoidance is usually associated with bank "A" and bank "C" not disclosing the final destination of the money, and thus bank "B" not being able to understand that the money is going to a sanctioned country.

In the case shown in the chart, Bank "B" is needed to convert the currency received for Iranian oil into U.S. dollars. Iranian oil may not be paid for in U.S. dollars due to sanctions.

This tactic has also been used to avoid sanctions in connection with the financial sanctions imposed on Russia. Often, in these cases, the funds go through countries that are not sanctioned and are not NATO members.

2. use of front or shell companies

To avoid sanctions, front companies and shell companies are often used to disguise the identity of the end users or the final destination of the money. Company forms that are easy to set up and allow the owner to be concealed are particularly suitable for this purpose. This applies in particular to the English corporate form of the limited partnership. This type of company consists of one or more general partners who are the owners of a company. However, these general partners can also be companies from abroad whose owners are not recognizable. A company address is then required for the opening, which can be located in a business center.

This company, represented by a salaried director, can conduct business in the United Kingdom. For example, real estate, works of art and luxury goods can be acquired without the private individual behind the company as financier becoming transparent.

In London, for example, many luxury properties were sold to Russian oligarchs, who have since been sanctioned, without the British authorities knowing anything about it. Some of these properties have now been seized in the course of investigations in connection with the sanctions imposed by the British government against Russia.

The strength of a sanction ultimately depends on the judiciaries and executives of those countries that must comply with the sanctions. Sanctioned persons will always look for ways and means to circumvent sanctions. In the past, they have often succeeded well. It remains questionable whether the judiciaries and executives will adapt better to sanctions in the future.

The effectiveness of the sanctions against Russia is still difficult to assess. So far, the EU has imposed a total of 748 sanctions and the USA even 1082 sanctions against Russian citizens, politicians, companies and the Russian Central Bank. On the one hand, the sanctions have resulted in a 9.7% drop in Russia's economic output, according to Statista. On the other hand, Russia's import performance from China is at an all-time high with growth of 23.7%. As long as China undermines the sanctions imposed by the West, there will remain a loophole for the Russian economy.

Sources:

Financial sanctions against Russia simply explained (finanzwende-recherche.de)

Matthew C. Klein on Twitter: "https://t.co/a5x7GNcwSF https://t.co/lCapgSiKEM" / Twitter

https://www.bundesregierung.de/breg-de/themen/krieg-in-der-ukraine/eu-sanktionen-2007964

h ttps://de.statista.com/infografik/26985/anteil-der-importe-russlands-aus-den-wichtigsten-lieferlaendern/

https://de.statista.com/themen/9109/sanktionen-gegen-russland/#topicHeader__wrapper